The Small Components Inside AI Servers, and the Big Money Behind Them

Some are already facing supply shortages, while others are still future expectations.

This is structural analysis, not investment advice. The companies discussed can be volatile, and the author may hold positions in some of the securities discussed. Readers should make their own investment decisions.

Same Wind, Four Sails

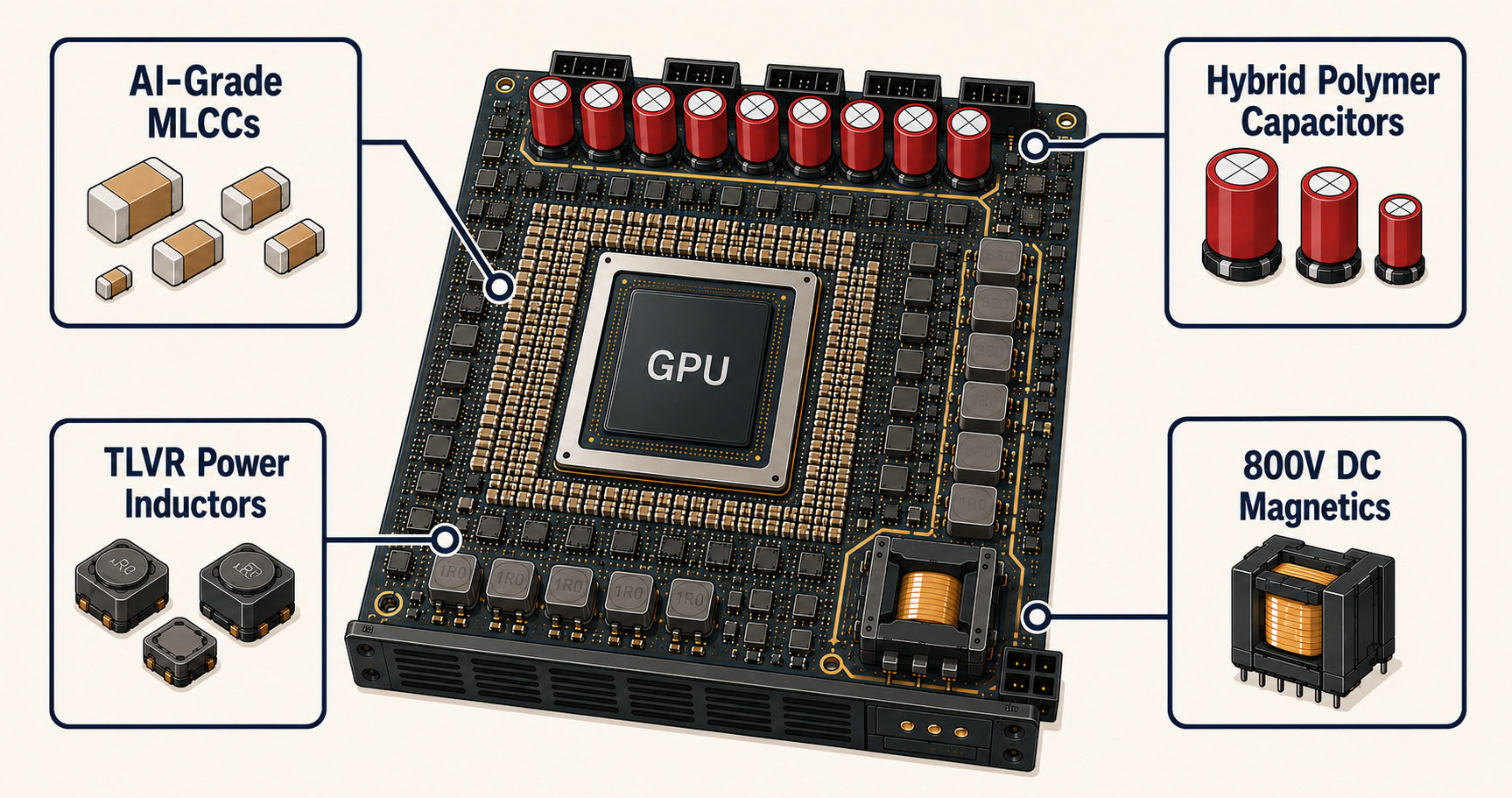

There is a component smaller than a fingernail: the MLCC, or multilayer ceramic capacitor. In a previous piece, I explained why this tiny part has become part of the AI power bottleneck. What AI GPUs demanded was not simply “more capacitors.” They demanded lower impedance. To meet that impedance target, designers had to place thousands of ultra-small capacitors right next to the GPU.

One NVIDIA NVL72 cabinet contains roughly 441,000 MLCCs. The next-generation GB300 is estimated to use tens of thousands of MLCCs per server. Public supplier references suggest that AI servers can require over 10x the MLCC count of general servers, with Samsung Electro-Mechanics citing 12.5x in one AI-server MLCC reference. The first questions in the comments under that piece were natural ones: “Samsung Electro-Mechanics?” “Murata?” In other words: who actually makes these parts?

![[MLCC] Why Does an AI Server Need 440,000 1mm Components?](https://substackcdn.com/image/fetch/$s_!PTS2!,w_280,h_280,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Ff2b54086-28a4-454f-8f08-90185847839e_1484x1060.png)

The visible answer

On April 30, 2026, part of the answer arrived in the market. Murata, for the first time, disclosed “Datacenter-related” revenue as a separate line item in its earnings materials. The guide was ¥325B, up 84% year over year. The stock was up ~200% over one year. On the same day, Samsung Electro-Mechanics reported ₩3.21T in quarterly revenue, up 17.2% YoY, and operating profit of ₩280.6B, up 39.9% YoY, with its stock up 271% year to date.

So far, the story feels intuitive. Parts demand explodes. The companies that make those parts go up.

The strange spread

But if we take one step back, something strange appears. MLCCs are not the only passive components inside an AI server. Capacitors, inductors, magnetics — different types of components all sit inside the same server. They broadly fall into four families.

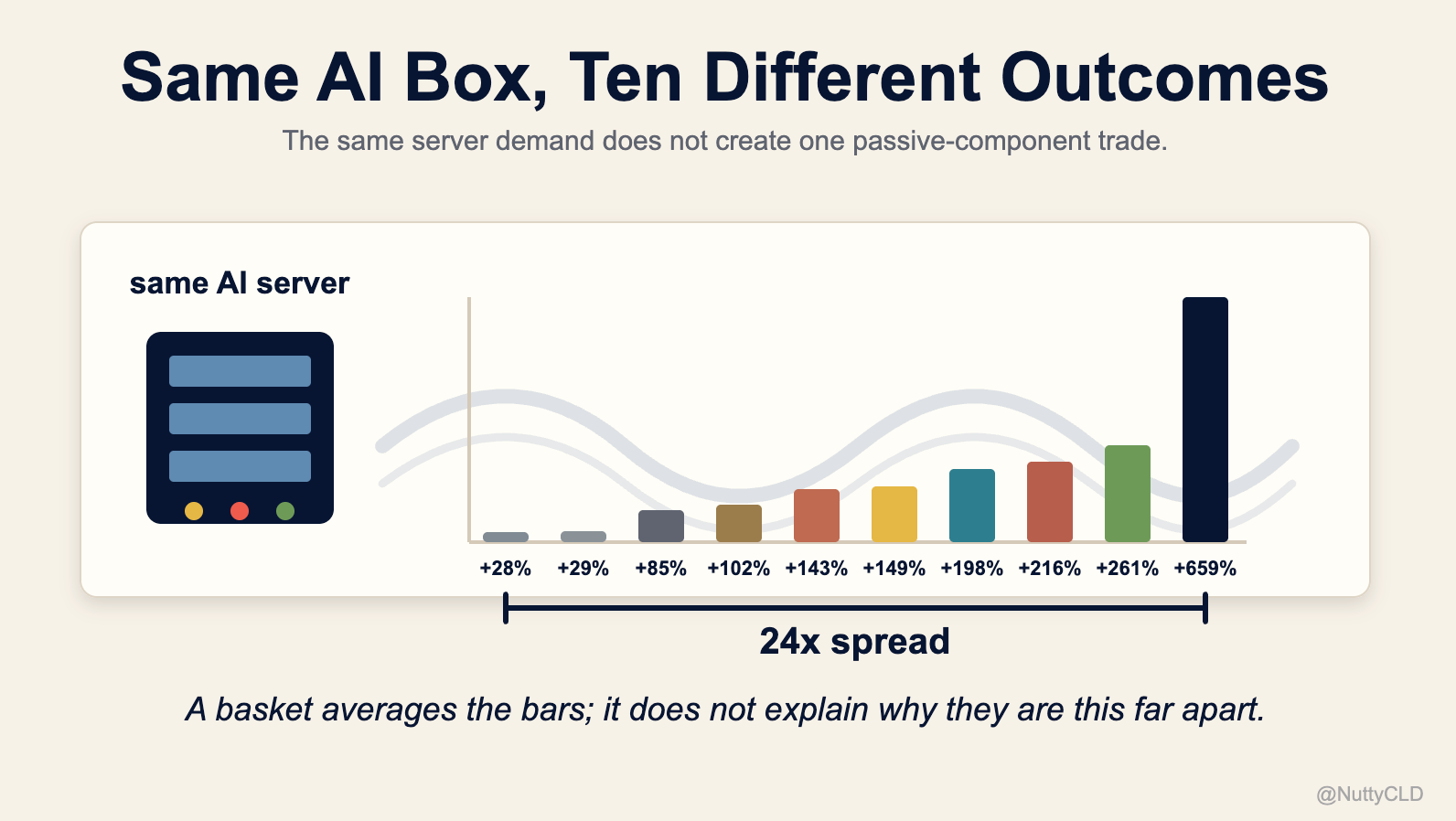

All four families are catching the same wind: AI server demand. But the public-market expression of that wind is uneven. Across the public names and proxies in the chart below, one-year returns range from +28% to +659%.

The stock-return gap alone is roughly 24x. That is where disclosure, visibility, and investor access start to matter.

The strange details do not stop there. In one family, a company’s stock is up 216%, yet the consensus target still sits at roughly one-third of the current share price. That means institutional models have not caught up. In another family, one of the clearest publicly documented specialists is private, so no ETF can really give investors clean access. In yet another family, no company has recognized revenue in the P&L yet. That story belongs to 2027 and beyond.

So what created this gap?

Technology alone does not explain it. Companies across this map can have meaningful technology in their respective niches, yet receive very different market treatment depending on what the market can actually see, model, and access. But the companies that have been re-rated most aggressively, such as Murata and Samsung Electro-Mechanics, share something beyond technology.

This piece breaks down each of the four component families and explains what that common thread is, and why it can move stock prices as directly as technology itself. Once we understand this common thread, we gain a lens that applies not only to AI passive components, but to almost every industry carrying the label “AI beneficiary.”

It also becomes clear why investing in “AI components” as a single basket can be dangerous. The timing of these four families is not the same. If one family rises in the same quarter another family falls, the basket cancels itself out internally.

And there is one company that appears across multiple parts of the map without being a pure-play winner in any single family. Its valuation becomes a useful cross-family reference for how the market is pricing the broader AI passives theme. A kind of cheat sheet. I will return to that later.

Within days, two of these four families are scheduled to report earnings. Whatever those reports show, they can be read through the framework in this piece.